One of my most recent encounters with the Romanian banking community was due to the Future Banking Summit, which happened this autumn. For 2 days in a row, together with my teammates managing banking and financial services projects in QUALITANCE, I listened to a world of ideas coming from bankers, fintechs, service providers, business consultants, and advertisers.

While the conference room got filled with hot topics like user-centricity, generative AI, KYC, automation, security, super apps, cloud-based solutions, UX, the most beautiful question only came up in the last panel. Can bank brands be truly loved? pondered Raluca Kovacs, Chief Strategy Officer from Publicis in a fireside chat with Costin Bogdan from McCann Worldgroup Romania.

The question stayed with me and got me thinking about others. What do banks need to do to gain that big customer love they strive so much for? Once they get it, how can they keep it? Because it’s not given. What makes customers give banks a cold shoulder? I’ll try to answer all of these questions with some of the insights gained at the summit, coupled with some of my own findings that fall under the same spectrum of thoughts.

Where do Romanians stand on banking

While the common bank portfolio embeds about 10 categories of products, from savings and checking accounts, certificates of deposits, loans and credit cards, investment and insurance products, online and mobile banking, merchant services and wealth management, according to a recent research from Kearney presented in the conference, Romanians apparently engage with only 2.2 banks and usually contract no more than 2 products or services.

With this in mind, I searched for what the other gaps in the Romanian market looked like and found that while 24% of Romanian employees are still paid in cash, 31% of Romanians in general do not have a bank account. Moreover, in 2023 the number of internet users in Romania stands at nearly 18 million, yet in 2022 nearly 5 out of 10 banking customers used the Internet Banking or Mobile Banking services.

Going back to the Future Banking Summit and all the ideas circling the air, one could notice the competition between banks and other banks, between banks and fintechs, between fintechs and other fintechs, adding new features, new services, new experiences, new technologies, better UX, better KYC, better mobility, better CX – and that is great! Regardless of who competes against who, the customer wins it all – as long as he or she or they are aware of what’s out there and they can make the most of it, fast and easy.

Going back to the answer to the first question, yes, both traditional bank and neobank brands can gain and keep that customer love if they do a consistent, better job as educators, as technology companies, as storytellers. Moving on, I’ll do some explaining for each role.

TYC matters just as much as KYC

Clearly, banks and fintechs are going out of their way to build outstanding and relevant experiences, yet the reluctant customer reaction to the latest developments in financial services across Romania summarized in the above-mentioned stats and facts may be due to a couple of reasons.

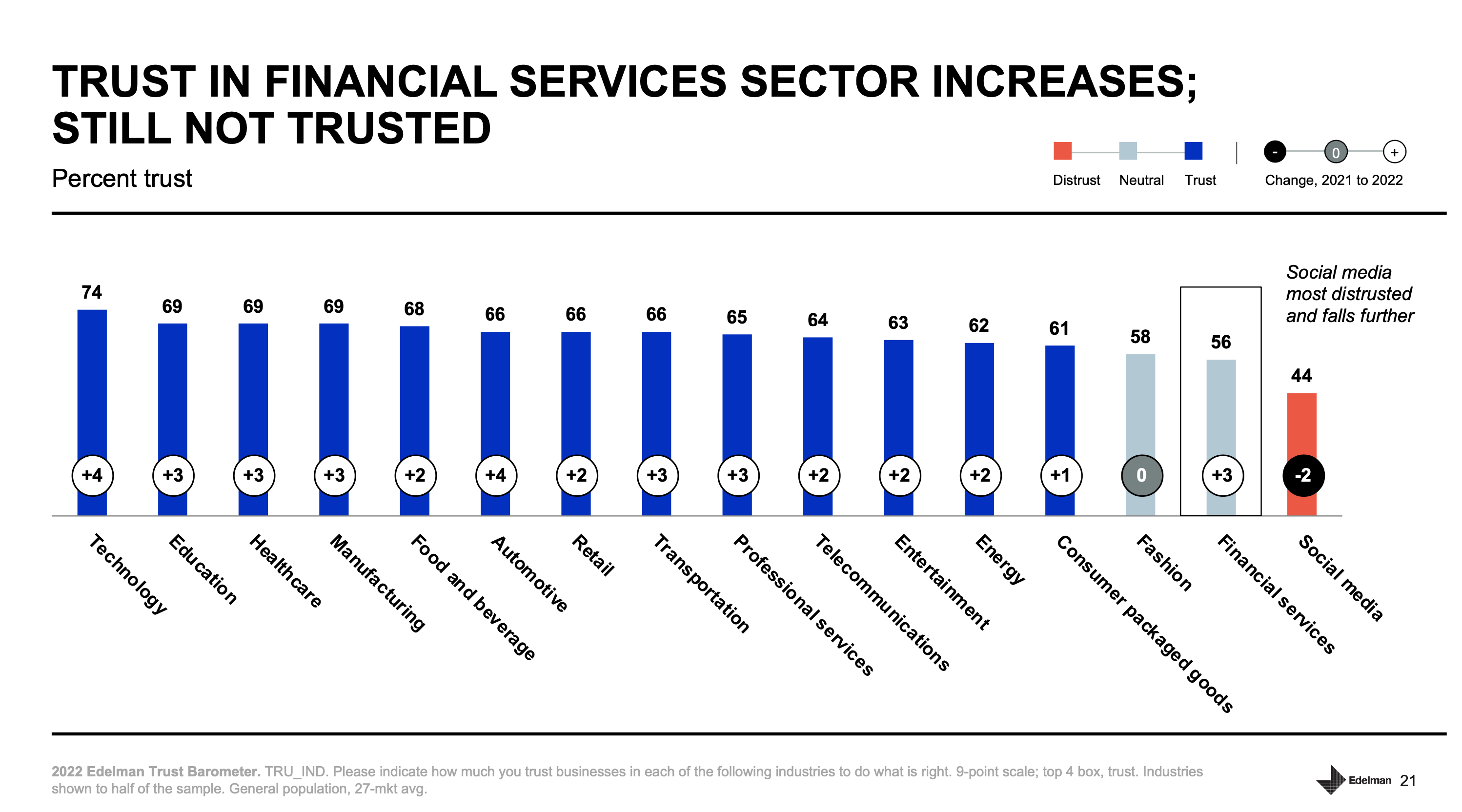

2022 Edelman Trust Barometer | Global Report – Trust in Financial Services Sector

- It can be that people in general are indifferent to financial services, yet in awe with technology, which they seem to trust most. If you take a look at Edelman Trust Barometer for 2022, you can notice the level of neutrality towards financial services is a global fact. Even though in 1 year financial services gained a 3-point increase, they’re still far behind every other sector, except for social media – which is most distrusted.

- It can be the paradox of digitalization. While it uses technology to create simplicity, the spiral of fast change adds complexity, as the human mindset cannot keep up the pace in rewiring – so we’re looking at a buffer or freeze period where adjustment and adoption of change takes longer.

- It can be that people in general do not like talking about money. It’s tabu. It makes them feel vulnerable and judged. On a side note, culturally speaking, Romanians are not comfortable talking about money since always. They don’t turn it into a conversation with their close ones, let alone with strangers such as banks. Hence, how fast can one internalize something that brings discomfort?

In each case, education makes a difference and it’s up to financial institutions to invest more in TYC (Teach Your Customer), by creating a natural space for conversation, by teaching them how they can make their own money work for their safety and confidence, and while they’re at it to speak and act human.

Giving Caesar what belongs to Caesar, if we look at the growing number of financial educational programs surfacing the local digital space, all leading banks in Romania have already stepped in the educator role, turning financial advisory, which used to be designed only for the wealthier segment, into a service available for regular people. Take, for instance, “The Money Chat” Podcast from Raiffeisen Bank, BCR Erste’s podcast “La Bani Marunti” advising regular people, or Banca Transilvania’s virtual and physical community for entrepreneurs – Stup.

All these educational programs that are engaging people into natural conversations about money, teaching them how to manage them and then grow some more are gradually building a human side to banks. They create space for relationships. They feel less institutional and more approachable. But there’s more they can do to grow an authentic, long-lasting relationship with customers.

Banks do not compete with (just) banks

A recent CX trends report from Zendesk reveals that banking customers don’t build up their expectations based on comparisons with other banks or other channels. They take their cues from the last best experience they had, regardless of industry.

This means banks do not compete with just banks anymore, they compete with Amazon, Netflix, Uber, Airbnb, TikTok, just to name a few. The precedent all these big players have created trandescends industries, making customers more demanding than ever. It doesn’t matter if you’re a bank, they won’t excuse you for taking too much of their time. They won’t show too much understanding for all your precautions, yet they will expect safety from you. They want you to know all about their needs and wishes, and act in their best interest, although they don’t enjoy your too-long, too-inquisitive KYC experience. They don’t want to repeat themselves over and over again, just because you don’t have all your data in one place.

Here’s a glimpse at what customers want, according to the above-mentioned Zendesk research:

- 72% of customers want immediate service

- 70% expect anyone they interact with to have full context

- 62% think experiences should flow naturally between both physical and digital spaces

- 62% agree that personalized recommendations are better than general ones

If starting conversations about money and teaching people how to make it work for them is humanizing banks, leveraging technology to refine the customer experience can truly increase their love of banks. It’s not just the automated onboarding that can make that a great impression, it’s also the safe hyper-personalization that can keep the customer close.

According to research from KPMG:

- 86% of consumers say that data privacy is a growing concern for them

- 68% are concerned about the level of data being collected by businesses

- 40% don’t trust companies to ethically use their data

- 30% aren’t willing to share their personal data for any reason

By combining predictive analytics, AI, and machine learning to monitor individual customers’ real-time usage data and by being transparent about how they process, use, and secure the customers’ data, banks can show good will and earn trust and these two conditions pave the way for long-term relationships.

Going back to the Zendesk report, one can only notice that none of the top customer expectations is achievable without cutting-edge technology, which like it or not remains the rockstar of any business pursuit (which needs all its CX & UX backing vocals”). Everything from efficient, omnichannel experiences to personalization and seamless integrations requires a total transformation that banks need to go through in order to make them possible. And in the process, financial companies, including banks, are gradually turning into tech companies, by choice or by pressure. The faster they encapsulate technology as the second new nature in their identity, the more solid the ground for a long-term customer relationship.

No Comments