With technology and demographics dramatically reshaping the payments value chain and fintech disrupting the financial world we find ourselves racing towards a cashless world.

According to McKinsey “Globally, electronic payments are a booming industry, having attracted more investment than any other financial-services sector and delivered the highest returns and growth in the sector over the past decade.”

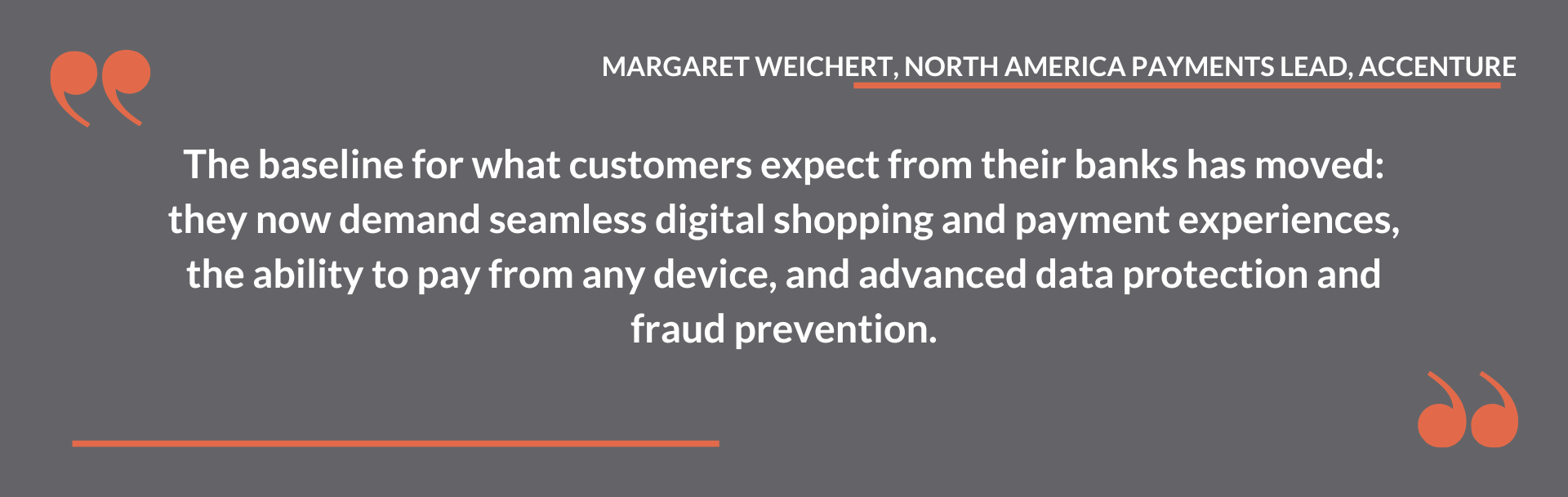

The main goal for the future, near and far? To facilitate transactions that are faster, safer, and simpler. Because that’s what customers, either individuals or corporate, are demanding – faster, more friction-free solutions.

A. Digital payments enter a new era of change

Tech innovation, customer behavior and interests, the current climate, but most importantly the influx of fintech funding are generating a boom in the “Payment Land”. Some sort of promised land that is currently developing and thanks to the pandemic influence (yes, it does hold its good parts) it is evolving at an even bigger scale than expected.

The Accenture report on “Growing payments to new heights” dives deep into 3 major disruptive forces that are creating change and opportunities for growth in the digital payment sector:

1. The launch of central bank digital currencies (CBDCs)

According to McKinsey, “roughly 90% of the world’s central banks are pursuing central bank digital currency (CBDC). Some, including those in the United States and South Africa, are at the exploratory phase; others are development projects (the European Union) and pilots (China).”

What’s to like about CBDCs? Well, they differ fundamentally from other forms of digital coins because they are directly backed by central bank deposits or a government pledge. “Therefore, they offer stable value and can aim to combine benefits in the areas of trust, regulatory stability, and audit transparency,” says McKinsey.

One of their most appealing features is that they can be held on physical devices such as cards or phone wallets, or simply exist as a digital book entry.

The same McKinsey points their finger at the slow pace of execution of the current processes in cross-border settlements. The CBDCs can act directly in reducing counterparty risk by enabling connected and instant settlement between parties.

2. The ever-changing customer behaviors and expectations

Customer needs change, and so do their behaviors. Top that with a global factor like the pandemic, and the curve of change gets faster.

The fintech sector can honestly credit the pandemic for its recent evolution and growth. This doesn’t mean we are not acknowledging its already blooming phase, but rather we are focusing on its latest, most encouraging drive: to cater to the changing behavior and expectations of customers in real time.

By creating new payment options like request to pay, digital currencies and buy now, pay later services (BNPL), fintechs have acted like a nurturing parent during the pandemic.

3. The adoption of new, emerging digital technologies

New digital technologies like AI or Cloud Computing are helping fintechs analyze their customers better and predict their needs and preferences. The aforementioned factors: behaviors and expectations are now easier to identify and meet. The result? An even smoother payment journey.

An agile technology facilitates faster go-to-market solutions tailored for a variety of needs. The Accenture report points out 3 key enablers in this respect:

- The Cloud as it enables payment providers to get to market faster with new value propositions;

- API platforms as they help integrate payments rails directly with customer platforms such as ERP systems or merchant point of sale systems.

- Data monetization since consumer data only becomes valuable once a payments company can use it to personalize customer experiences and influence commerce.

All these new technologies, digital currencies and the ever-changing economic and political environment are driving change in the corporate payments space also.

Creating a seamless flow between a brand’s physical and online stores and its needs diverse, complex payment solutions. Nothing new here, but making it possible and coherent in real-time is tricky.

“Corporates must ensure that enterprise resource planning (ERP) platforms/posting systems and reporting systems are current and equipped with adequate technology supporting the technical changes required for all systems to accommodate this new world order, as well as the human resources needed for this new age.” – Shanker Ramamurthy, Managing Partner, Global Banking & Financial Markets, IBM Consulting.

B. A taste of fintech payment platforms

It seems harder and harder to remember the world before payment platforms. Especially when the total transaction value in the Digital Payments segment is projected to reach US$8.49tn by the end of 2022, out of which US$933.10bn is forecast to come from the EU countries (Source: Statista).

Around the world, various fintech payment platforms are trying to rule a world where the word “cash” is starting to become obsolete. Some of them are real mammoths, some are not that big in size, but have a better focused target.

1. VISA

Visa is and will probably remain the peak of the mountain in matters of digital payments. In addition to its credit and debit cards, Visa also operates electronic funds transfer (EFT) through its division – Interlink.

2. Ayden

Less known, but equally important, Ayden’ story started in 2006 in the Netherlands, a country which prides itself to be a cashless leader in Europe. It offers end-to-end payments, data, and financial management in a single solution. In 2021, it registered €516 billion in processed volume.

3. Klarna

Based in Sweden, Klarna story starts in 2005. Its core service is to provide payment processing services for the e-commerce industry, managing store claims and customer payments. It has also implemented a (BNPL) service provider, offering customers credit on their purchases as part of the checkout process.

4. Finstro

An Australian-based fintech company that started solving financial challenges within the B2B trade since 2014. Lead by the motto “Let FinStro do it”, the company is offering a wide variety of payment solutions to pay and get paid on terms that suit your business.

5. Checkout.com

This UK-based cloud-based payments platform offers a full stack of payments solutions. Through their modular technology the customers can seamlessly add the features they need, manage risk and fraud, and add new payment methods to support their growth in multiple new markets.

With electronic payments gaining more and more ground, with cryptocurrency and digital currencies acting as emerging forces, our beliefs and attitudes about money are rapidly and surely changing.

Anne Boden, founder and CEO of Starling Bank, the British digital challenger bank which provides current and business accounts, advanced the idea that “in a post-pandemic world, it is likely that digital payments will become increasingly popular and widely used. However, in our eagerness to make money quicker, faster and better, we must be careful not to exclude the most vulnerable people around us.”

Our needs are shaping the future and the way things are developing at the moment, digital payments are getting embedded into our lives. Whether supported by favorable demographics, economic growth, innovation or even a pandemic, our needs dictate the way we trade, we buy, borrow or save money. Simply put, how we actually live.

No Comments